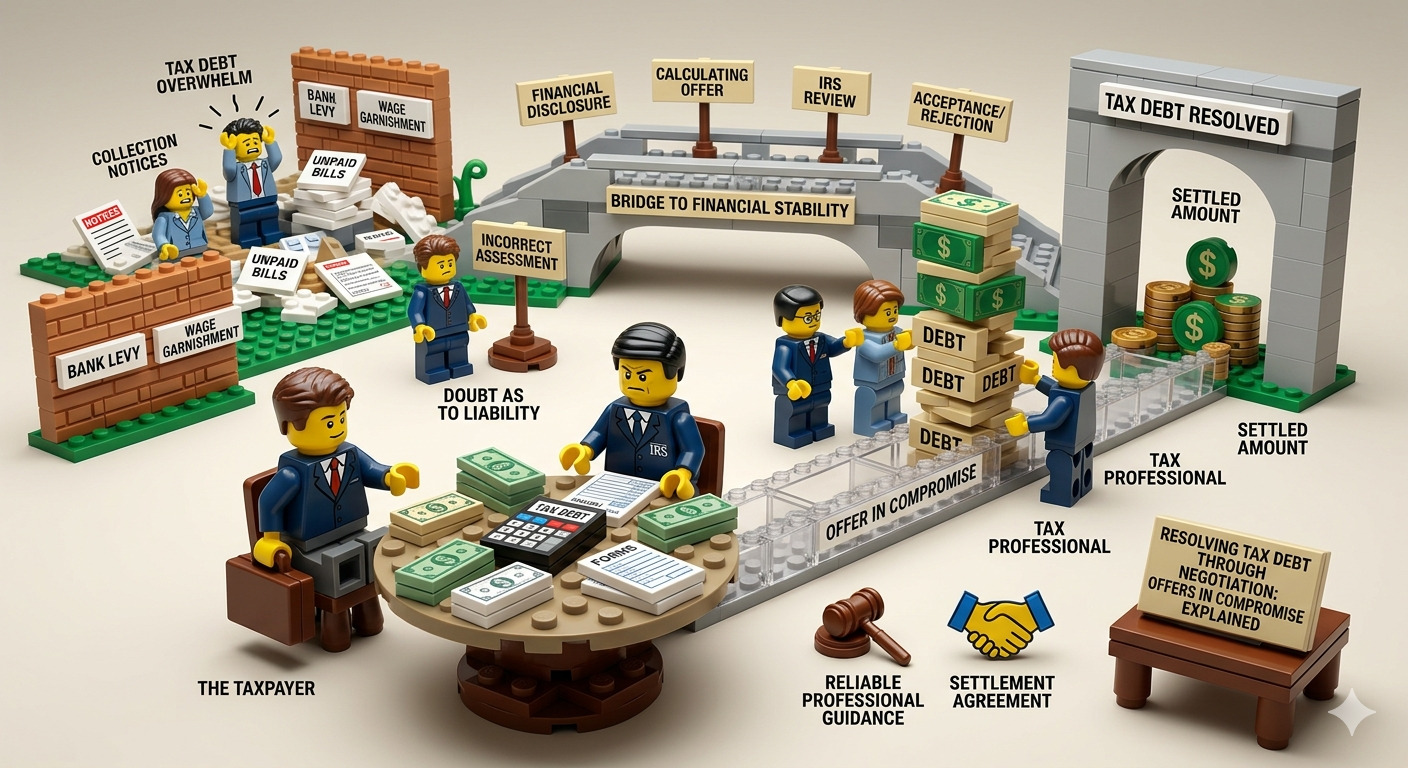

When Tax Debt Becomes Overwhelming

Owing money to the IRS can quickly become one of the most stressful financial situations an individual or business may face. What begins as a missed payment, unexpected tax bill, or filing mistake can grow rapidly as penalties and interest accumulate.

Many taxpayers initially try to handle the situation themselves by ignoring notices, delaying payment, or hoping the issue will resolve over time. Unfortunately, tax debt rarely disappears on its own. In fact, unresolved balances can eventually lead to serious collection actions such as tax liens, bank levies, wage garnishments, or the seizure of business assets.

The good news is that the IRS offers legitimate programs to help taxpayers resolve their debts when full payment is not financially possible. One of the most well-known options is an Offer in Compromise (OIC).

An Offer in Compromise allows certain taxpayers to negotiate and settle their tax debt for less than the full amount owed. However, the process is complex and requires careful preparation. Understanding how the program works — and whether you qualify — can help prevent your situation from escalating into more serious collection problems.

This guide explains what an Offer in Compromise is, how the program works, and when it may be a viable solution for resolving tax debt.

What Is an Offer in Compromise?

An Offer in Compromise is a formal agreement between a taxpayer and the IRS that allows the taxpayer to settle a tax liability for less than the full amount owed.

The IRS considers an OIC when it believes the taxpayer cannot realistically pay the full balance through normal collection methods. Instead of pursuing the full amount indefinitely, the agency may accept a reduced settlement that reflects the taxpayer’s true ability to pay.

In other words, the IRS may agree to accept a lower payment if it determines that collecting the full amount is unlikely.

However, approval is not automatic. The IRS carefully evaluates each application to determine whether the offer represents the maximum amount it can reasonably expect to collect.

Why Taxpayers Consider an Offer in Compromise

For taxpayers facing substantial tax debt, an OIC can provide a path toward financial stability.

Some of the most common reasons individuals and businesses pursue this option include:

- Significant financial hardship

- Income that is insufficient to pay the full tax balance

- Accumulated penalties and interest that exceed the original tax owed

- Long-term financial limitations due to illness, unemployment, or business loss

For eligible taxpayers, settling the debt through negotiation can offer relief from the stress and uncertainty of ongoing IRS collection activity.

However, because the IRS closely scrutinizes these applications, careful preparation is essential.

How the IRS Determines Eligibility for an Offer in Compromise

The IRS evaluates several financial factors before deciding whether to accept an offer.

The agency’s goal is to determine the taxpayer’s reasonable collection potential — essentially, how much the IRS believes it can collect through normal enforcement actions.

To make this determination, the IRS reviews:

Income

The agency examines current and projected income from all sources, including wages, self-employment income, rental income, and investment earnings.

Assets

Taxpayers must disclose all assets, including:

- Real estate

- Vehicles

- Bank accounts

- Retirement accounts

- Investments

- Business assets

The IRS evaluates the equity in these assets when determining whether a settlement is appropriate.

Monthly Expenses

The IRS also reviews a taxpayer’s living expenses, including housing, transportation, utilities, food, and medical costs.

However, the agency uses standardized guidelines for many expense categories, meaning not all personal expenses may be fully considered.

Future Ability to Pay

Even if a taxpayer cannot pay the full balance today, the IRS considers whether the individual may be able to pay more over time.

This evaluation helps determine whether a settlement offer represents the most the IRS can reasonably expect to collect.

Types of Offers in Compromise

The IRS generally considers three types of Offers in Compromise.

Doubt as to Collectibility

This is the most common type of OIC.

It applies when the taxpayer’s financial situation makes it unlikely that the IRS will ever collect the full amount of the tax debt.

In these cases, the IRS may accept a reduced settlement amount that reflects the taxpayer’s actual ability to pay.

Doubt as to Liability

This type of offer applies when the taxpayer disputes the accuracy of the tax debt itself.

For example, the taxpayer may believe the IRS calculated the liability incorrectly or that the assessment was based on incomplete information.

Effective Tax Administration

In rare cases, a taxpayer may technically be able to pay the full debt, but doing so would create severe economic hardship.

In these situations, the IRS may consider a settlement based on fairness and equity.

The Offer in Compromise Application Process

Applying for an OIC involves a detailed financial review and submission of specific documentation.

The process generally includes several steps.

Step 1: Financial Disclosure

Taxpayers must provide a comprehensive overview of their financial situation, including income, assets, expenses, and liabilities.

This information allows the IRS to evaluate the taxpayer’s ability to pay.

Step 2: Calculating the Offer Amount

The settlement amount proposed must reflect the taxpayer’s reasonable collection potential.

If the IRS determines that the offer is too low based on financial disclosures, the application may be rejected.

Step 3: Submitting the Application

The completed application package typically includes:

- Financial disclosure forms

- Supporting documentation

- Application fees

- An initial payment toward the proposed settlement

Submitting incomplete or inaccurate information can delay processing or lead to rejection.

Step 4: IRS Review

The IRS carefully reviews the application, verifies financial information, and determines whether the proposed offer represents the maximum it can reasonably collect.

This review process can take several months.

During this time, collection activity is generally paused while the offer is under consideration.

Step 5: Acceptance, Rejection, or Negotiation

After reviewing the application, the IRS may:

- Accept the offer

- Reject the offer

- Request additional information

- Propose a different settlement amount

Taxpayers may also have the opportunity to appeal certain decisions.

Why Many Offer in Compromise Applications Are Rejected

Although the program can be effective for qualifying taxpayers, many applications are denied.

Common reasons for rejection include:

- Incomplete financial documentation

- Understated income or undisclosed assets

- Offers that are lower than the IRS’s calculated collection potential

- Failure to remain current on tax filings and estimated payments

Careful preparation and accurate financial analysis are essential when pursuing an OIC.

How Resolving Tax Debt Early Prevents More Serious Problems

One of the biggest mistakes taxpayers make is waiting too long to address their tax debt.

When balances remain unpaid, the IRS may initiate increasingly aggressive collection actions.

These can include:

Federal Tax Liens

A tax lien is a legal claim against a taxpayer’s property, which can affect credit, business operations, and the ability to sell assets.

Wage Garnishments

The IRS may require employers to withhold a portion of wages to satisfy the debt.

Bank Levies

Bank levies allow the IRS to seize funds directly from bank accounts.

Asset Seizures

In more severe cases, the IRS may seize vehicles, business assets, or real estate.

Understanding resolution options, such as an Offer in Compromise, allows taxpayers to address their debt before enforcement actions occur.

Other Tax Debt Resolution Options

An Offer in Compromise is not the only solution available.

Depending on the taxpayer’s situation, other options may include:

- Installment agreements

- Temporary hardship status

- Penalty abatement requests

- Structured payment arrangements

Evaluating these options carefully ensures the chosen strategy aligns with the taxpayer’s financial reality.

The Value of Professional Guidance in Tax Debt Negotiations

Tax debt negotiations involve complex financial analysis and detailed communication with the IRS.

Professional representation can help taxpayers:

- Evaluate whether an Offer in Compromise is realistic

- Prepare accurate financial disclosures

- Structure settlement offers strategically

- Respond to IRS requests during the review process

- Explore alternative resolution options if necessary

Early involvement of a qualified professional often improves the likelihood of a successful outcome.

Take Action Before Tax Debt Escalates

Tax debt can feel overwhelming, but ignoring the problem only increases financial pressure over time.

Programs like the Offer in Compromise exist to help taxpayers resolve liabilities when full payment is not possible. However, navigating the process requires careful planning and a clear understanding of IRS expectations.

Addressing tax debt early can help prevent liens, levies, and other serious collection actions that may disrupt your financial stability or business operations.

Learn Whether an Offer in Compromise Is Right for You

If you are struggling with tax debt, exploring your options for resolution is the first step toward regaining control of your financial future.

An Offer in Compromise may allow you to settle your tax liability for less than the full amount owed — but determining eligibility requires a thorough financial review.

Learn whether an Offer in Compromise is the right solution for your tax debt. Contact us today for an assessment and take the first step toward resolving your IRS obligations.