-

The IRS “Fresh Start” Program: It Doesn’t Exist

There is not now and there never has been an IRS Fresh Start Program. None. Nada. If anyone tells you different, they’re selling false hopes of utopia and you’re the prospective payor. Let’s start with a bit of background. The IRS started using the optimistic and somewhat friendly sounding catchphrase “Fresh Start” with a brief…

-

IRS Certified “Collection Notices” – A Complete 2025 Guide

If you’re expecting to see a listing and detailed description of every kind of certified mail that the IRS might ever send, well, consider yourself saved. The primary and most important consideration is that if a professional has not been consulted prior to receipt of a certified letter on any particular matter or issue, the…

-

Tax Collection Defense – Quick Guide & FAQ

It’s difficult to imagine a less-welcome telephone call, letter, or notice than one coming from an IRS Revenue Officer or IRS Collection Office (particularly from “ACS”, the Automated Collection System). Think about it. The job of IRS Collection personnel, all day long, is to get money from people who mostly aren’t real excited to hear…

-

If I Cash Out My 401(k), Can It Be Garnished? – Protecting Retirement Accounts from IRS Collections

The IRS can obtain an interest in retirement vehicles like 401(k)s and IRAs. Once an assessment has been made against a taxpayer, the IRS gives the taxpayer notice of the assessed amount and demands payment. The initial notice and demand is, in effect, a bill for taxes due. If the taxpayer fails to pay the…

-

Will I Lose My Tax Refund if I File Chapter 7?

Filing for bankruptcy can be complex, especially regarding your tax refund. If you’re considering Chapter 7 bankruptcy, you might wonder what will happen to that much-needed tax refund. Let’s go ahead and dive into the details and explore your options. When you file for Chapter 7 bankruptcy, a court-appointed trustee distributes your non-exempt assets to…

-

Clearing Tax Debt with Bankruptcy: Quick Guide & FAQs

All About Clearing Tax Debt with Bankruptcy The bankruptcy code does not specify which tax claims can be eliminated; instead, you determine which tax claims are not dischargeable. Below is a summary of the general rules surrounding the discharge of income tax claims (although other types of tax claims may also be eliminated in bankruptcy).…

-

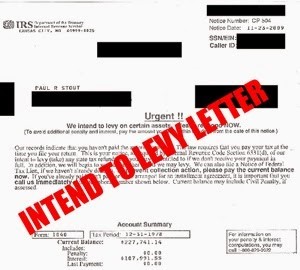

Notice of Intent to Levy – What Purpose Does It Really Fulfill Or Is It Just A Scare Tactic?

In addition to the requirements of proper notice and demand, two different notices of intent to levy are required. First, §6331(d) requires that the IRS notify the taxpayer in writing of the IRS’s intention to levy on the taxpayer’s salary, wages, or other property, at least 30 days before the date of the levy. In…